WHICH FICO® SCORE MODEL IS USED?Today, mortgage lenders use classic FICO scoring models for mortgage applications. FICO created slightly different scoring models for each credit bureau. They are:

FICO® Score 2,

FICO® Score 2, or Experian/Fair Issac Risk Model v2

FICO® Score 5,

FICO® Score 5, or Equifax Beacon 5

FICO® Score 4,

FICO® Score 4, or Transunion FICO Risk Score 04

Mortgage lenders get a single "tri-merge" credit report that contains your credit reports from each of the three bureaus and associated credit scores. Most programs will use the middle score (ignore the highest and lowest). If you are applying jointly, the lowest middle score is used.

NEW CREDIT SCORE REQUIREMENTS COMING SOONIn Octobert 2022, the Federal Housing Finance Agency (FHFA) announced significant change to the credit score requirements for mortgage loans. Estimated to begin in the fourth quarter of 2025, lender will only have to provide the newer FICO 10 T and VantageScore 4.0 scores.

Both of these newer credit scores are calculated based on the information in one of your credit reports. However, the models may be more predictive and consider types of data that weren't as widely available when older models were created. For example, FICO 10 T and Vantage Score 4.0 can consider rental payments in your credit file and trends in your credit history, such as how your credit utilization ratio changes over time. They also treat medical collections differently then older versions and ignore paid collection accounts.

DO ALL MORTGAGE LENDERS USE THE SAME CREDIT SCORES?Mortgage lenders are currently required to provide the classic FICO

® listed above when selling mortgage loans. However, there are some non-conforming and jumbo loans that may require or allow different scoring models to be used. It's always best to know your credit scores when applying for a mortgage!

WHAT IS A GOOD CREDIT SCORE TO BUY A HOUSE?The higher the credit score, the higher likelyhood of available loan programs. This guide shows the minimum credit score requirements for the different loan programs. Remember, in addition to the minimum score, some loan programs may require other items to be present within your credit profile.

| Mortgage Type |

Minimum Credit Score |

| FHA with Down Payment Assistance |

600 |

| FHA with 3.5% Down Payment |

580 |

| FHA with 10% Down Payment |

500 |

| USDA with 0% Down Payment |

580 |

| VA with 0% Down Payment |

500 |

| Conventional Loans (min 3% down) |

620 |

| Jumbo Loans |

660 |

WHAT ELSE DO LENDERS LOOK AT?Your credit scores are an important factor in getting pre-approved to purchase a home and also dictates the interest rate you will receive. However, other factors are considered in the approval:

Credit History: Even if you meet the min credit score requirements, you might still be denied due to your credit history. Some important factors include recent (anything within 2-3 years) bankruptcy, foreclosure, late payments and collections. Any open disputes may be required to be resolved as well.

Employment and Income: You will need to provide acceptable employment history for the prior 2 years with no large gap in between employers. If self employed, must have minimum of 2 years of tax returns with acceptable taxable to income to meet debt-to-income (DTI) requirements.

Assets and Reserves: Even if qualifying for a zero down or down payment assistance loan program, you may be required to provide reserves (essentially liquid assets that are shown but not used). One month reserve is the amount equal to one monthly mortgage payment.

Other factors, such as the loan amount, household income (for all members even if not a borrower) and borrower(s) total income can play a factor into the loan approval depending on the program and product you are requesting. It's important to inquire about all possible loan programs that you may be interested in.

HOW TO IMPROVE YOUR CREDIT SCOREAlthough there are differences in the credit score calculations, the classic FICO

® Scores and the newer scoring models will only consider information in one of your credit reports. As a result, similar actions might help increase all your scores.

Some of the things you can do to improve your credit:

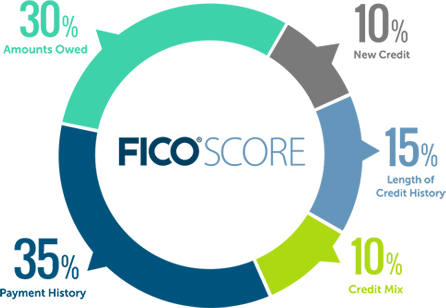

Reduce credit card balances: This is typically the quickest way to increase your credit score. 30% of your score looks at your credit utilization as the chart below shows.

Paying your debts on time: Even missing one payment can dramatically hurt your credit score. Make sure to pay all your bills on time, even those not reporting on credit.

Don't apply for other types of credit: Avoid applying for loans or credit cards if you are thinking about buying a home. Credit inquiries can lower your credit score and opening new debt could affect the amount of your pre-approval due to increasing your DTI.

Monitoring your credit is also important to ensure everything reporting is accurate. Disputing any inaccurate accounts can also help boost your credit score. A premium credit monitoring service that also provides the classic FICO

® Scores version is essential. Myfico.com is one of the most popular. Click the link below to start monitoring your credit today.